Monte Carlo Portfolio Simulation - Probability Forecasting & Risk Analysis

A Monte Carlo simulation that estimates the probability of an investment portfolio reaching a target value over a multi-year horizon, and quantifies the full range of possible outcomes.

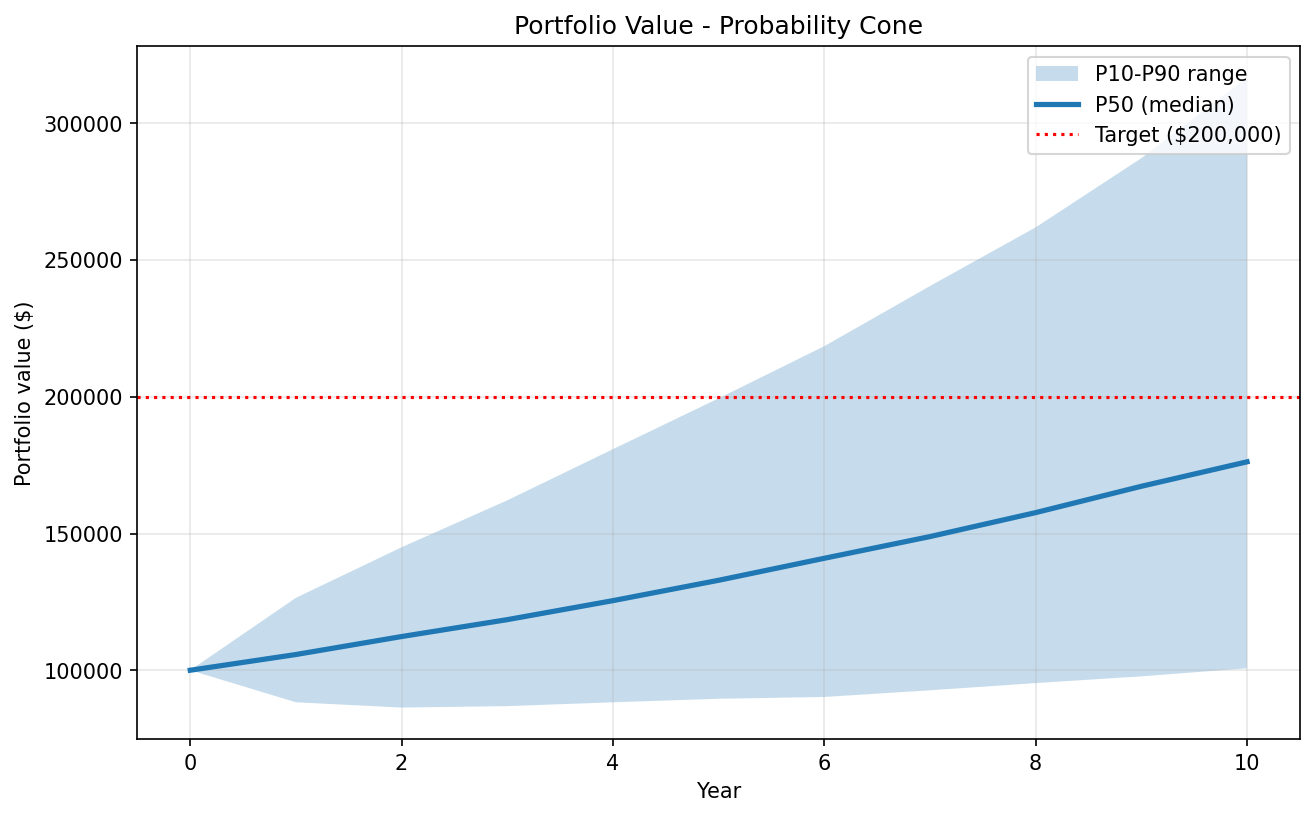

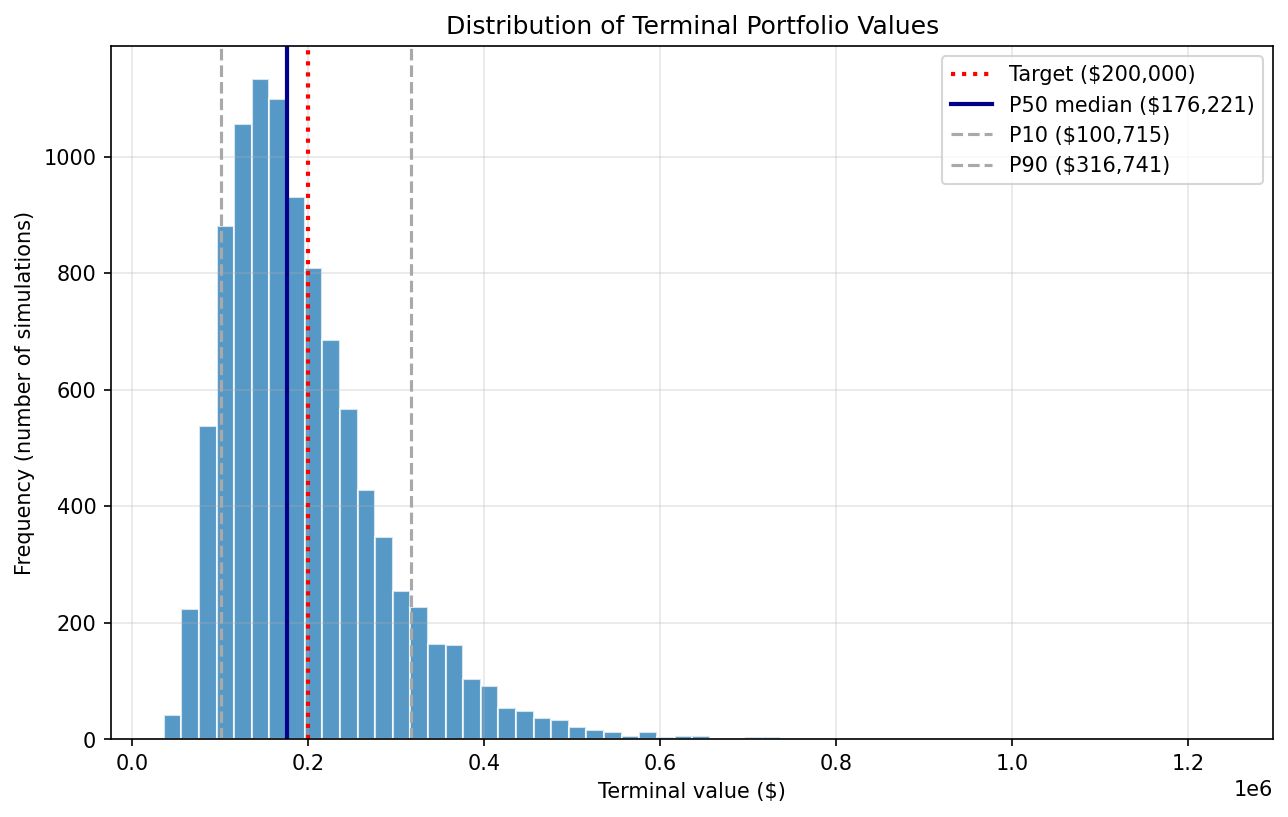

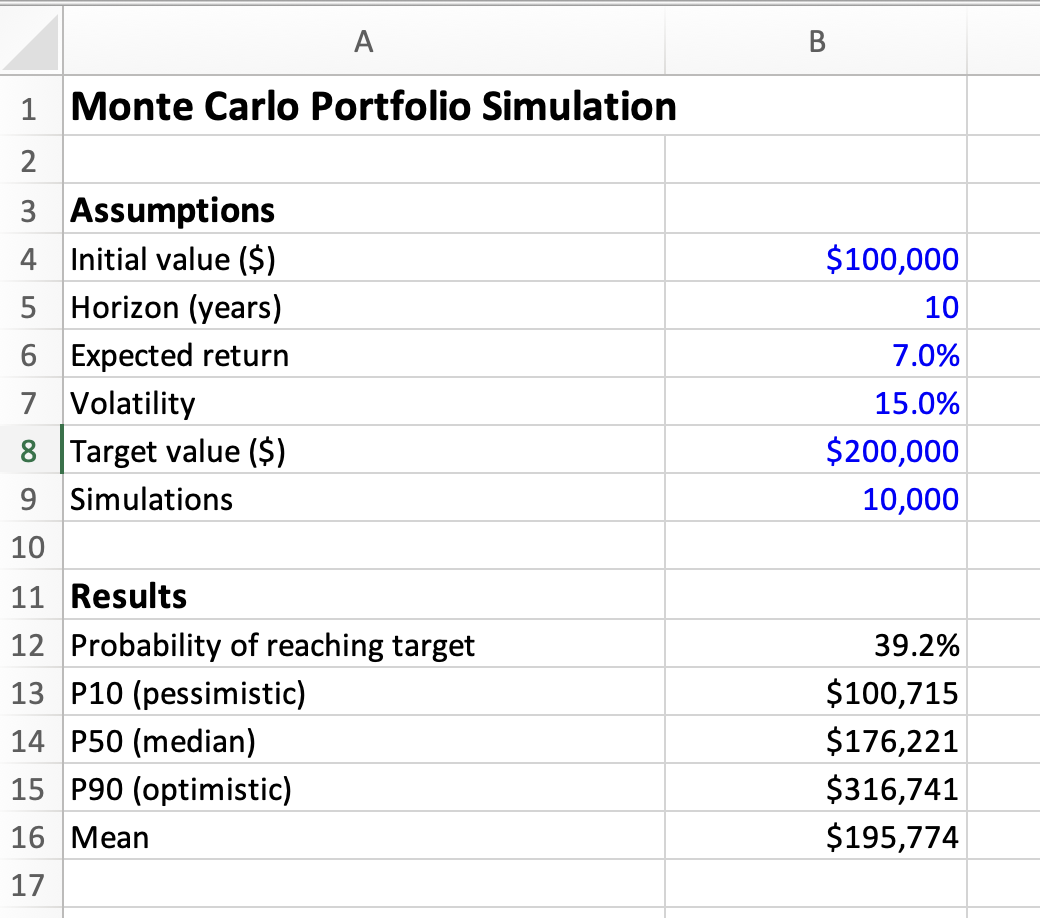

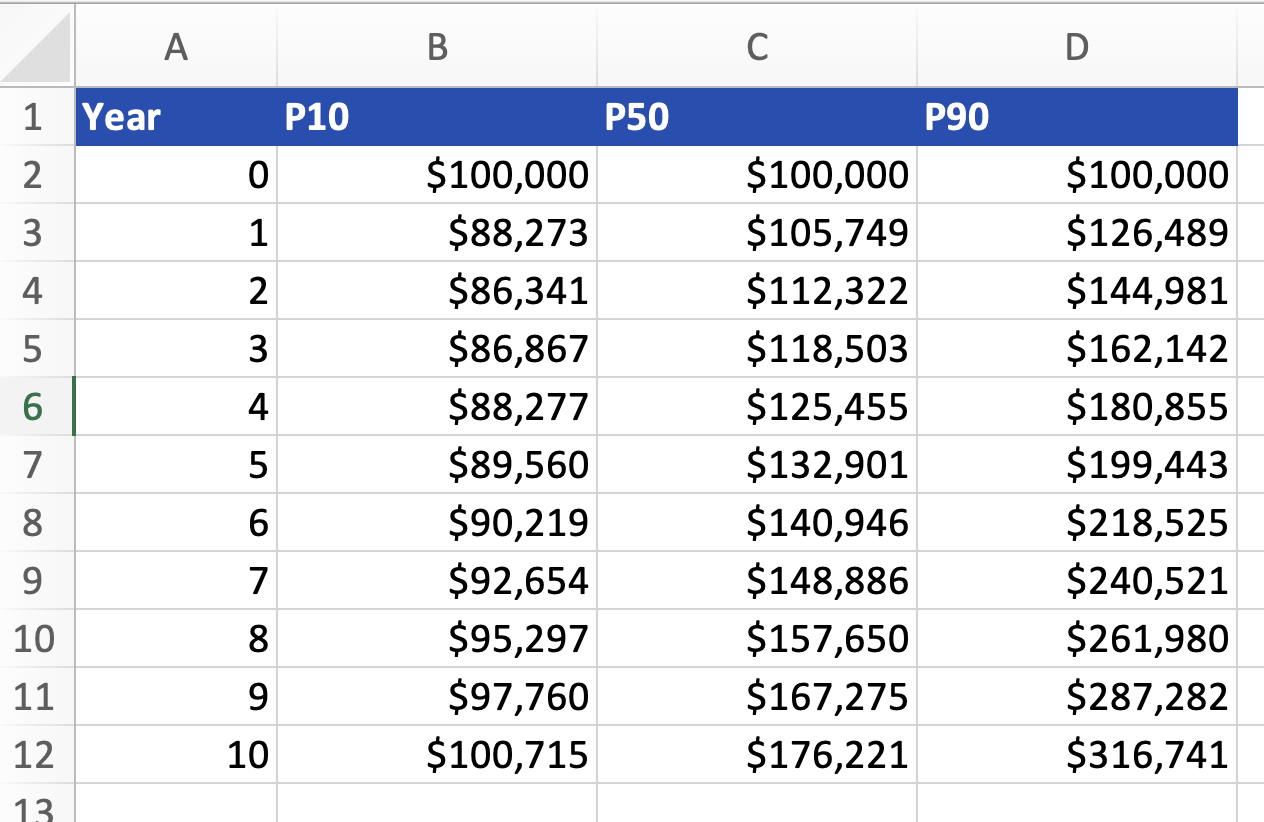

The model runs 10,000 simulated paths using a lognormal return process, producing the probability of reaching a target, P10/P50/P90 outcome bands, a probability cone showing how outcomes widen over time, and a terminal-value distribution. Results are delivered in a clean, formatted Excel workbook with embedded charts and a methodology note.

Built with: Python, NumPy, Matplotlib, openpyxl